Surajit Das

.

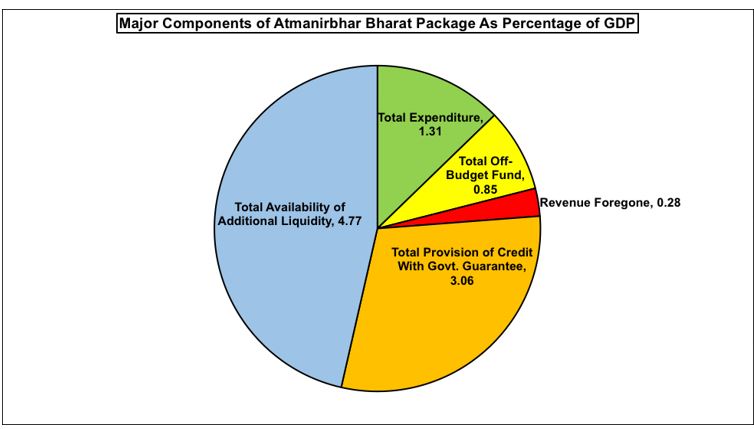

There were a lot of announcements about the reform measures in the Finance Minister’s speech in five parts following the Prime Minister’s address. However, we are not going into the details of those here. Let us just look at the numbers which have been presented as part of Atmanirbhar Bharat package of Rs.20 lakh 97 thousand and 53 crores, which is 10.28% of India’s GDP for the year 2019-20. For our understanding, all the heads have been divided into five broad categories viz. expenditure from the government exchequer, off-budget funds, revenue foregone, credit with government encouragement and liquidity injection (see the graph below).

As far as the expenditures of the government of India are concerned, the PM Garib Kalyana Yojana was announced earlier with an allocation of Rs.1 lakh 70 thousand crores, which is 0.83% of the GDP. An additional amount of Rs.40 thousand crores have been allotted to MGNREGS and Rs.15 thousand crores have been allotted for the health sector as per the PM’s announcement. Rs.10 thousand crores have been allocated for micro food enterprises, and Rs.2800 crores have been allocated for employees’ provident fund. Rs.4 thousand crore for promotion of herbal cultivation, Rs.1.5 thousand crores for interest subvention for MUDRA Sishu Loans, Rs.5 hundred crores for operation green and another Rs.500 crore has been allocated for the Beekeeping initiative. For the purpose of free food grain supply to the stranded migrant workers, an additional allocation of Rs.3500 crores have been made. Including all these, the total additional government expenditure would be in the tune of Rs.2.48 lakh crores, which is around 1.2% of GDP.

.

There is an existing scheme called the PM Matsya Sampada Yojana. An extra allocation of Rs.20 thousand crores has been made in Atmanirbhar package for this scheme. Including that the total expenditure would be Rs.2.68 lakh crore or 1.3% of GDP. There is a proposal of creating four new funds called agri infrastructure fund (Rs.1 lakh crore), animal husbandry infrastructure development fund (Rs.15 thousand crore), funds of fund for MSMEs (Rs.50 thousand crore) and viability gap funding (Rs.8100 crore). However, these are off-budget items and the contribution of the government in these funds is not mentioned – together they constitute Rs.1 lakh 73 thousand crore or 0.85% of the GDP. The TDS/TCS rates would be reduced by 25% and the approximate tax revenue foregone due to this would be Rs.50 thousand crores. Due to some tax concessions, the additional revenue loss since March 22nd is Rs.7.8 thousand crores. So, the total revenue foregone would be around Rs.58 thousand crores or 0.28% of the GDP. Including government expenditure, fund building for agricultural infrastructure and revenue foregone, the total size of the package is in the tune of 2.44% of GDP.

.

The rest of the 7.8% of GDP amount of the package is all about credit (3% of GDP) and liquidity (4.8% of GDP). Collateral free credit of Rs. 3 lakh crore with government guarantee and additional credit of Rs.2 lakh crore through Kishan Credit Card have been announced. Rs.20 thousand crores additional credit to MSMEs on account of subordinate debt for stressed MSMEs would be provided subject to the demand. Additional emergency working capital of Rs.30 thousand crores would be provided to the farmers through NABARD. Housing credit would be boosted by Rs.70 thousand crores and special credit facility of Rs.5 thousand crores would be provided to the street vendors. Therefore, the additional expected credit offtake by the MSMEs, farmers and street vendors is worth of Rs.6 lakh 25 thousand crores, which is 3.06% of GDP.

.

As far as the liquidity measures are concerned, through various steps of the RBI, the expected availability of additional liquidity would be around Rs.8 lakh crore or little less than 4% of GDP. Apart from this, there is an announcement of liquidity injection of Rs.90 thousand crores for the electricity distributing companies against their dues. There is a partial credit guarantee scheme of Rs.45 thousand crores for liabilities of non-banking financial institutions and micro finance institutions and special liquidity scheme of Rs.30 thousand crores for them and for the housing finance companies in the country. Reduction in EPF rates from 12% to 10% is expected to enhance liquidity by Rs.6750 crores. Reduction in TDS rate or EPF contribution of employees from their current income would enhance the current disposable income in their hands, which may generate some more additional demand in the economy.

.

However, lower EPF contribution means lower savings unless the government contributes that 2% on behalf of the employees – but, there is no such proposal as of now. If we add these with the potential liquidity injection by the RBI, the total liquidity measure comes to the tune of Rs.9.73 lakh crore, which is 4.77% of GDP of 2019-20. The essential assumption is that this much extra credit would be demanded and actual additional credit offtake would be equal to this to stimulate the economy. But, that would never be the case in a demand depressed situation. In fact, the aggregate supply of liquidity is always demand-driven and credit-led.

.

It is important to remember here, although both availability of extra liquidity as well as expected credit by the MSMEs and the farmers have been added to arrive at Rs.21 lakh crore number, there is substantial overlap and hence double counting. These MSMEs and farmers would take the loan with government guarantee from the commercial banks, NBFCs, NABARD etc. who have been enabled to extend extra credit. From the point of view of investment, growth and employment generation, the money would be invested by the MSMEs and the farmers once and not twice. Even if we believe that out of total Rs.9.7 lakh crore additional loanable fund, they take Rs.6.25 lakh crore amount of extra loan using government guarantee and make investment and the rest of the loanable fund is borrowed by others (unrealistically assuming full credit offtake) without government guarantee, then the total increase in investment would be of Rs.9.7 lakh crore and not of Rs.16 lakh crore, which is supposed to boost the economy and enhance the aggregate level of activity. If we calculate this way, avoiding the potential double counting, the size of the package according to the government’s own calculations and definitions would be only of 7% of GDP and not more than 10% of GDP.

.

Obviously, under a depression like this, it is unlikely that the actual credit offtake would be equal to the availability of liquidity with the banks and the NBFCs. If there is no profitability, the investors would not demand for credit without which credit cannot be supplied. In order to boost aggregate demand in the market, the purchasing power of people have to be enhanced. However, the point is that even after a catastrophe of this scale, our government has announced a fiscal stimulus package with merely 1.3% of additional government expenditure if the expenditure of other departments and schemes are not reduced to finance this additional spending. Hope, there would be another package to revamp MGNREGS and expand it to the urban areas and to enhance the government health spending substantially as proportion of GDP and so on to boost the aggregate demand in the economy soon. Fiscal conservatism would prove to be treacherous now under the current situation.

.

The author is Assistant Professor at CESP, JNU, New Delhi