Satyaki Roy

Satyaki Roy

Given addressing the ‘long pending’ labour market reforms, besides introducing the four Labour Codes related to wages, occupational safety, industrial relations and social security there has been state-level interventions in recent times to water down existing labour laws to the extent of suspending Minimum Wages Act, 1948. Behind the political and legal controversies that such moves triggered off, what seems to have brewed for quite some time is an unfounded belief that India’s manufacturing growth has largely been hindered by the absence of labour market flexibility, which in so many words, was arguing for freedom of employers to hire and fire and delegitimise all institutional protections ensuring fair wage. The crux of the argument perhaps relies on two well-entrenched faiths rather than informed wisdom: one, a fall in wage will ensure higher employment and second, lower-wage of workers will, in any case, increase the competitiveness of Indian products in the global market. The former proposition essentially ignores the fact that the worker is both producer and consumer and although for an individual employer it is completely rational to try and push down wages in reducing costs, but for the economy as a whole a fall in wages also implies a reduction in the number of buyers, hence a fall in aggregate demand that may cause a rise in unemployment rather than employment. More importantly at the level of an individual employer, the decision to employ an additional worker is not driven by the level of wages but the additional return that the employer may derive from the newly employed worker at reduced wages. In other words, if the employer finds that producing more by recruiting new people is going to fetch higher returns through the expanded market, then only it is rational for the employer to engage more workers at lower wages. Given the fact of huge unutilized capacity in Indian manufacturing, rising unemployment and gloomy consumer sentiment, lowering of wages does not seem to be a good enough incentive for the employer to employ more workers. Instead, the employers are more inclined to squeeze existing workers by way of extending working hours, reduce wage costs through substituting older workers by lesser number of new entrants, delegitimize collective bargaining and dissent and also remove existing provisions of health and occupational safety. Essentially the untold path, therefore, is of reducing compensation costs as a means to achieve global competitiveness.

Trends in Manufacturing

There are two distinct stylized facts in the world of manufacturing. Firstly, during the period 1990 to 2016 global manufacturing value added at constant 2010 prices doubled and the share of developing and emerging economies increased significantly. Secondly, the share of manufacturing in world GDP and for three-fourths of the countries in the world including China, the share of manufacturing shows a declining trend in their respective GDPs. True indeed that most of the countries are reaching the peak share of manufacturing much faster and at a lower share of GDP. This perhaps implies that even though the world of value addition is undergoing a structural change nevertheless, the current phase of globalisation apparently provides opportunities to developing countries in increasing their share in enhanced global manufacturing value-added. But taking advantage of emerging possibilities varies according to appropriate strategies adopted by respective countries in increasing their capabilities. During the period 1994-2015 India could increase its share in global manufacturing value-added from 1.1 per cent to 2.8 per cent while China increased its share during the same reference period from 5 per cent to 25 per cent of global manufacturing value-added. Within the group of developing and emerging industrial economies India’s share was 7.7 per cent while China’s share reached 54.6 per cent of the group’s total manufacturing value added (Hallward-Driemeier and Nayyar, 2018). It is also important to note that the rise of China as the manufacturing powerhouse of the world roughly coincides with the period when Chinese wage shows a rising trend.

No denying the fact that relocation of manufacturing facilities from global North to the global South is largely driven by the fact of taking advantage of labour arbitrage and lax environmental regulations prevailing in the South. According to the latest figures available of international comparisons of manufacturing compensation costs, Chinese wage is only 11.3 per cent of the US wage and that of India is 4.4 per cent of the same. This huge difference in compensation costs between the developed and developing economies is, of course, the most important reason for the relocation of manufacturing towards the global South. But within the group of developing countries higher share in manufacturing value-added cannot be explained by low labour costs alone. There are various dimensions of competitiveness and the UNIDO comes out with a competitive industrial performance index (CIP) for 148 countries giving a relative measure of the competitiveness of these countries in the global market. According to this index of 2015, China’s rank is third after Germany and Japan and India’s rank is 39 although India’s wage is less than half of Chinese wage in the manufacturing segment.

It is also important to note in the context of relocation of manufacturing to developing countries in general and in connection to ‘make in India’ and India’s integration to global production network in particular, industries relocated from advanced countries are not necessarily labour intensive in nature. As capital costs decline sharply in advanced countries, industries have undergone a substitution of labour by capital where it can be done easily, but for sectors where the elasticity of substitution is low, are the ones relocated to developing countries where the labour is relatively cheap. That does not, however, mean that these sectors are labour-intensive according to developing country standards. In fact, the major global integration happened in the case of India are the sectors such as electrical machinery, optical equipment, transport equipment, motor vehicles, fabricated metal products, chemicals and non-chemical mineral products are all medium-skilled relatively capital intensive sectors. And competitive edge on these sectors does not actually depend upon low compensation costs rather on innovation, adaptation and skills.

Wages and Employment in Asia

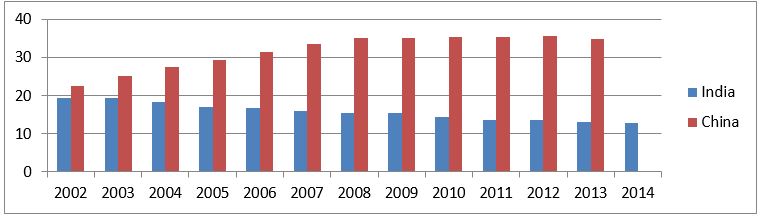

Transforming farm labour into unskilled workers of labour-intensive manufacturing had been the usual route of industrialisation at the initial stage of structural change for most of the early industrialising countries. The Chinese path in the beginning of reform in 1978 was driven by labour-intensive export-led manufacturing making use of cheap labour whose wage at that time was three per cent of the US wage and even less than the prevailing wage in Philippines and Thailand. But more importantly, China didn’t actually rely upon the low level of wage as such. Instead on the dramatic fall of the unit labour cost which is wage as a percentage of labour productivity that fell very sharply during the entire decade of the 1980s and in mid-1990s reached as low as 30 per cent of the US unit labour cost. In other words, there was a sharp rise in productivity of Chinese workers while the wages continued to remain low and thereafter manufacturing wages picked up only since the late 1990s. It is important to note that the meteoric rise of China in the global landscape of manufacturing exports roughly coincides with the period 1998 to 2010 when Chinese real wage increased at an annual rate of 13.8 per cent. China seemed to have reached its Lewisian turning point in 1998 when wages increased at all levels, skilled or unskilled, high growth coastal areas or in non-coastal areas, for exporting or non-exporting firms. This was primarily because of the demographic shift, slowing down of labour force growth and the decline of the growth of migrant workers. In fact, in many Chinese provinces particularly in the coastal areas, there have been signals of acute labour shortage for the first time reflected by the fact that newly created jobs were greater than the number of job seekers (Li et al, 2012). Figure 1 and 2 shows the compensation costs and share of social security expenditure for India and China over the years.

Figure 1: Manufacturing Hourly Compensation Costs in India and China, US Dollars

Source: International Comparisons of Hourly Compensation Costs in Manufacturing database, ILC

Despite having a real wage growth rate even faster than the growth of GDP, China tops in low skilled labour-intensive manufacturing exports, fourth in medium skill exports and the topmost exporter in high-skill manufacturing goods in the world.

Figure 2: Manufacturing Employer’s Social Insurance Expenditures as Percentage of Total Compensation Costs

Source: same as Figure 1

India had a distinct but a very short phase of high growth in non-farm employment during the period 2000 to 2012 when 7.5 million jobs were created annually in the non-farm sector mostly driven by construction boom absorbing 4 million workers every year. But the process was cut shortly thereafter. The number of new non-farm employment during 2012-2018 fell sharply to 2.9 million annually with construction and manufacturing absorbing only 0.6 million each (Mehrotra, 2020). Consequently, there was a rise in rural and urban wages of regular workers during 2004-05 to 2011-12 which declined in 2018 and the rise of the wages of casual workers also slowed down subsequently.

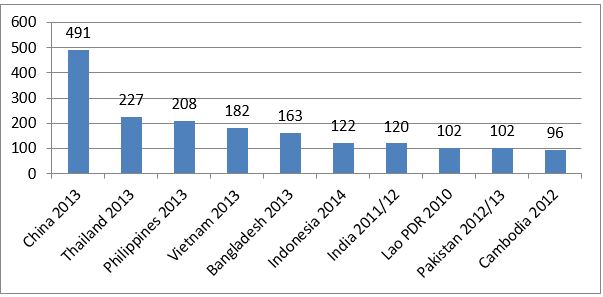

If we see the labour-intensive industries such as textiles, garments and footwear, there also the trade volume and international competitiveness do not depend only on the level of wages. According to an ILO study of 2014 done to compare performance in these sectors, Asia Pacific region excluding Arab states accounts for 59.5 per cent of global exports of garments, textiles and footwear in which China’s exports was the highest of 358 billion dollars followed by India with 42.7 billion dollars and Vietnam exporting worth of 37 billion dollars. Figure 3 shows the comparable average wage rates in these sectors where the Chinese wage is more than four times of what Indian workers receive on an average in these sectors.

Figure 3: Average Nominal Monthly Wages in Garments, Textiles and Footwear

Source: Wages and Productivity in the garment sector in Asia and the Pacific and the Arab States, ILO, 2016

India’s average wage in these industries are even less than that in Indonesia, Bangladesh and Vietnam because workers are mostly employed in the factory sector in these countries while in India these sectors are overwhelmed by own account enterprises and family workers.

Wage-Productivity and Global Competition

Competition in the global market is determined by relative unit labour cost of a country in a particular industry. Broadly speaking unit labour cost is the share of wages to labour productivity. Essentially it implies that if the productivity of the worker increases faster than the growth of real wages then unit labour cost falls and the country assumes a greater competitive edge. It can be shown that unit labour cost is directly related to real wages, the ratio of the price of wage goods to the price of the output and inversely related to labour productivity. Therefore, with rising real wages a country can reduce or contain unit labour cost if the productivity of the workers increases faster than wage rise or keeping the real wages unchanged, it can decline also if the ratio of wage goods to the price of output can be reduced. This explains the apparent paradox that six of the top ten global exporting countries of labour-intensive goods in the world are advanced countries where wage levels are much higher than the emerging economies. Their unit labour cost is low because of higher labour productivity. The East Asian countries also adopted the trajectory of enhancing labour productivity through investment in fixed capital and subsidized learning. In the case of China during the period 1997-2010 labour productivity showed an annual growth of 11.3 per cent. Recently with the rise in real wages faster than labour productivity China experiences rise in unit labour costs in various segments particularly because of the enhanced minimum wages declared in 2004. As a response, China is moving towards producing more high-skilled products supported by a mission to have 40 per cent of the workforce with a college degree by 2050.

Lowering wage and competing for a larger share in the global market in matured products is highly unsustainable particularly because wages rise faster than labour productivity in segments like garments, textiles and footwear and producers in these footloose industries easily move out to other countries where wages are relatively low. Particularly in these segments the scale of production matters as larger scales reduces average costs and for new entrants competing with established global players becomes difficult. Moreover, for newly industrialising countries these segments have been the launching pad of industrial transformation. As the number of new entries increases competition among developing countries ultimately leads to a ‘race to the bottom’ reducing return from additional units of exports. The fact is capital intensity in India’s manufacturing is already on the rise and its globally integrated manufacturing operations as mentioned earlier are not at all labour intensive in nature. In such a scenario competition should be based on increasing productivity by investing more on R&D and building up a healthy and educated workforce. On the contrary, the excitement on relaxing labour laws and abandoning all sorts of protective rights in the name of competition seems to be a covert attempt to informalise manufacturing employment in view of reducing wages. Notably, the average productivity of workers in the informal manufacturing sector in India is roughly one-seventh of that of their formal counterparts. Therefore, overarching concern on squeezing labour would ultimately lead to a downward spiral of low productivity and low wage because maintaining a lower unit labour cost with falling productivity would perpetually require pushing down real wages. This, in any case, would be counterproductive in attaining higher share of exports in sectors that India seems to have engaged where investment on R&D, innovation and skills are more important determinants of competitiveness than wages of workers.

The author is Associate Professor at ISID, New Delhi

References

Hallward-Driemeier, Mary and Gaurav Nayyar 2018. Trouble in the Making? The Future of manufacturing Led Development, Washington: The World Bank Group.

Li, Hongbin Lei Li, Binzhen Wu and Yanyan Xiong 2012. ‘The End of Cheap Chinese Labor, The Journal of Economic Perspectives, Fall, 26 (4), 57-74.

Mehrotra, Santosh 2020. ‘Industrial Strategy with Employment Policy for Job Creation’ in Mehrotra (ed.) Reviving Jobs an Agenda for Growth, Penguin Books.